“Stocks get the pixels, bonds get the dollars,” wrote my colleague Sylvester Flood in Morningstar’s Global Fund Flows report earlier this year. It’s a paradox, to be sure. For years, a technology-powered equity market captured the popular imagination and produced incredibly strong returns, while bonds vexed investors. Yet, between 2015 and 2024, fixed-income funds and exchange-traded funds captured nearly $5 trillion in global flows. Their equities-focused counterparts brought in “just” $2.7 trillion. Strong bond fund flows have continued into 2025, too.

Investor appetite for fixed income has persisted even during years of low yields, 2022’s “worst bond market ever,” an inverted yield curve, and recent inflation fears. Demographics could be part of the story. Aging investors moving from the accumulation to decumulation life stage shift into more conservative, income-producing assets. “Widespread rebalancing to policy allocations because of equities’ hearty returns” is the hypothesis proffered by Morningstar’s fund flows report. So, selling stocks and buying bonds could be about maintaining a target allocation—60/40 for example.

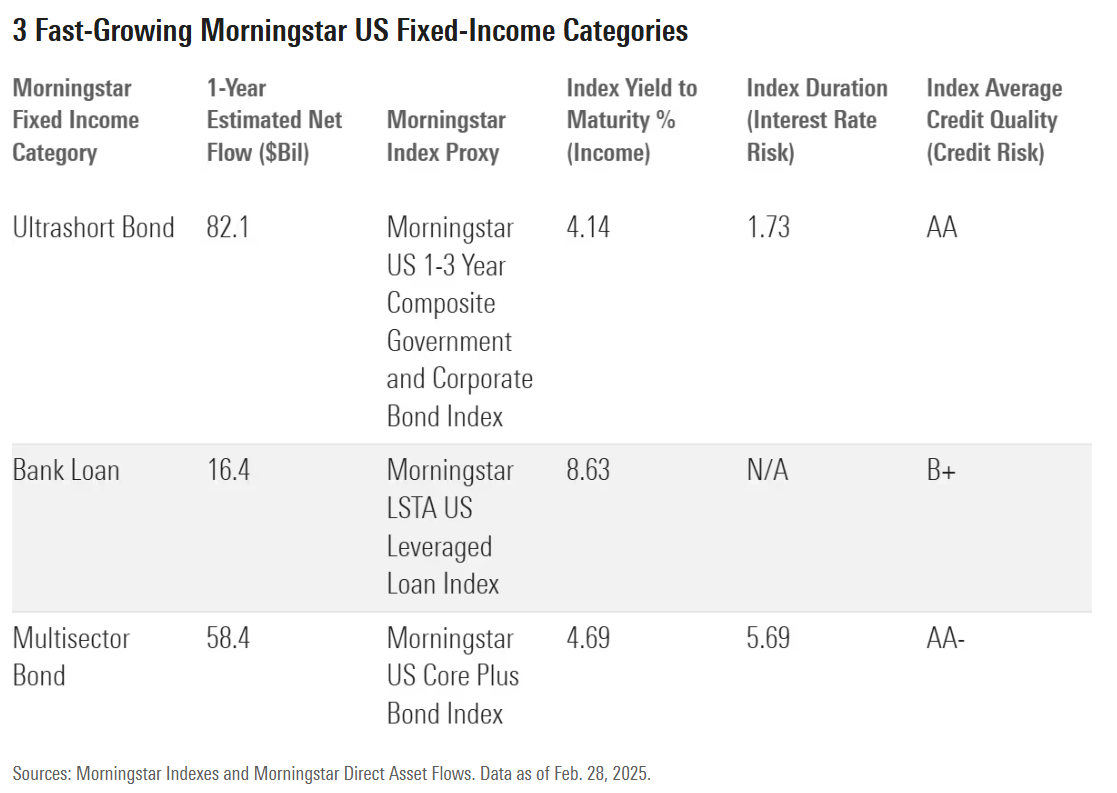

Whatever the reasons, it’s worth examining the areas within fixed income attracting the most flows. Investors are flocking to a diverse group of categories—from conservative ultrashort bond funds to far riskier bank loans to wide-ranging multisector strategies. Each category is unique from the perspectives of income, risk-return, and diversification. Below is a table with key stats, a short discussion of each category, and thoughts on their pros and cons in the current market context. I’ll use Morningstar fixed income indexes as proxies, but fund-specific research is also required.

Ultrashort Bond

Investors have poured into funds and ETFs in the US ultrashort bond category, including nearly $30 billion of net inflows in the first two months of 2025. Undoubtedly, a big part of the story here is a flight to safety in a highly uncertain environment. Yields are also decent. The Morningstar US 1-3 Year Composite Government and Corporate Bond Index, which can be used to proxy the category, had a yield of 4.14% as of February month-end. That’s not much lower than strategies with significantly greater interest-rate risk. The Treasury yield curve inverted again in February 2025, making cash and short-term bonds higher-yielding than some longer-dated bonds. In contrast to cash though, ultrashort bond funds have total return potential. That could be a plus if the Federal Reserve resumes cutting rates but can also work against investors. In 2022, for example, the index declined 4%.

It’s important to recognize that the ultrashort bond category isn’t monolithic. Adam Sabban and Ryan Jackson of Morningstar Manager Research note a band of “red-hot ETFs” focused on collateralized loan obligations. These strategies could behave differently than Treasury-heavy funds.

Bank Loan

Once a niche asset class, syndicated bank loans have found an investor base. As represented by the Morningstar LSTA US Leveraged Loan Index, the loan market has surpassed that for high-yield bonds in size. It’s a relevant comparison because the two asset classes both take on considerable credit risk. In contrast to high-yield bonds, though, loans have floating-rate coupons, so the steep interest-rate hikes that started in 2022 did not undermine their prices. In fact, the Morningstar index declined less than 1% in 2022, then saw its yield climb into the double digits in 2023. Income is clearly a big point of appeal for funds in the bank loan category, with a current yield of nearly 9%.

The “convergence” of public and private markets is another aspect of the bank-loan growth story. Many borrowers are backed by private equity, and collateralized loan obligations are big buyers of the loans. Leveraged loans are related to private credit and are often used to proxy that asset class. Credit investors, including those looking to park “dry powder” while waiting for a private credit allocation to take shape, find leveraged loans a convenient way station.

Multisector Bond

“Between traditional higher-quality core bond and riskier high-yield corporate-bond funds lie strategies that offer investors a diversified approach to income generation with higher risk-adjusted return potential,” writes Paul Olmsted of Morningstar Manager Research. Funds in this category like to juice things up with high-yield bonds and emerging-markets debt, in addition to more “core” investment-grade fare. Looking at the funds in this category that are highly regarded by Morningstar’s Manager Research team, they tend to employ a large toolkit and give their managers significant leeway.

Investors piling into this category are likely income-hungry. The Morningstar US Core Plus Bond Index, which is an imperfect proxy, has a solid current yield. Some funds in the category throw off significantly more income. The trade-off, of course, is credit risk. In a downturn, a portfolio with exposure to high-yield bonds and nonagency mortgages could see losses well beyond those of more staid strategies.

Some Fixed-Income Strategies Diversify Better Than Others

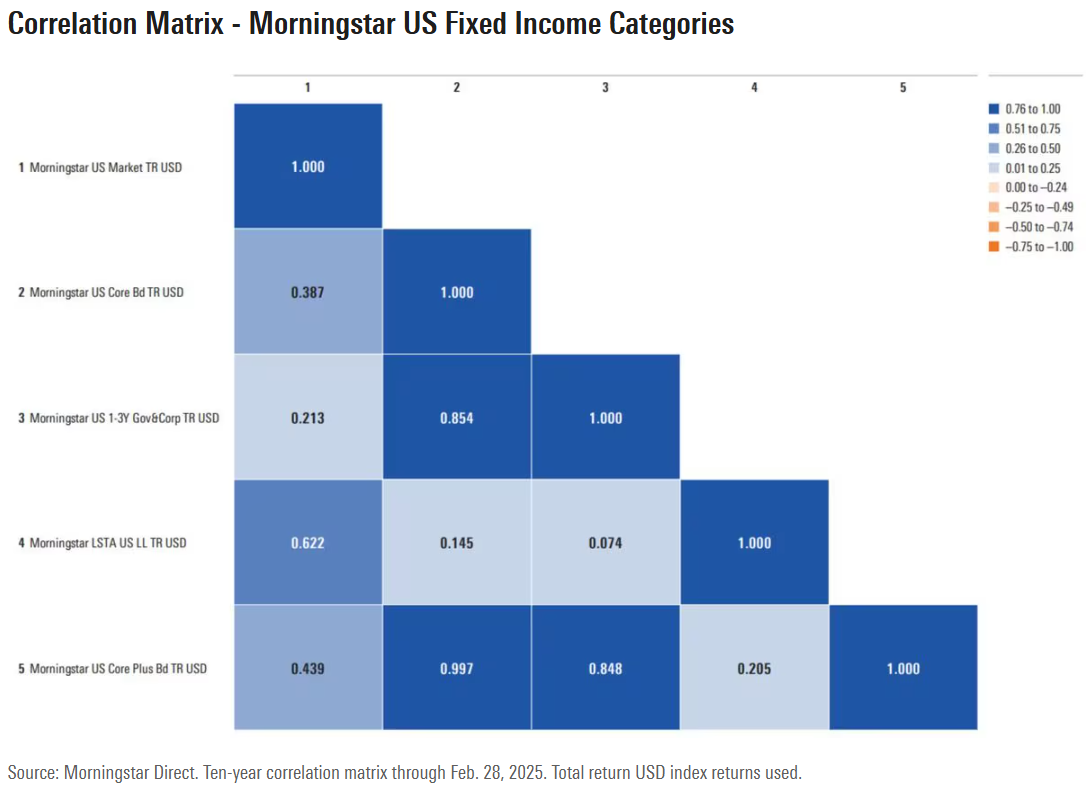

Portfolio diversification is another key aspect of fixed-income investing. Bonds are known as “ballast” to an equity-heavy portfolio because they are less volatile and tend to steady the ship during stormy waters. High-quality bonds, especially Treasury’s, have an attractive habit of going up when equities are going down. The Morningstar US Core Bond Index, which represents the investment-grade debt universe, gained value during several equity market selloffs this century, including the aftermath of the dot-com bubble (2000-02), the global financial crisis (2007-09), and the “pandemic panic” of 2020’s first quarter. The relationship broke down in 2022, though, when inflation and sharp rate hikes prompted double-digit losses for both stocks and bonds.

What kind of diversification benefits do today’s popular fixed-income asset classes offer? The below correlation matrix displays each index proxy’s relationship to the Morningstar US Market Index, a broad gauge of equities, as well as to the Morningstar US Core Bond Index. It encompasses a 10-year period that includes up and down markets for both stocks and bonds.

Of the three popular fixed-income categories, the Morningstar US 1-3 Year Composite Government and Corporate Bond Index—representing the ultrashort bond category—is the least correlated to equities. In fact, its behavior has diverged even more from the equity market than has the core bond index. As you’d expect, the Morningstar US Core Plus Bond Index—representing the multisector bond category—is more correlated to equities than a portfolio of bonds that are entirely investment-grade rated.

The Morningstar US LSTA Leveraged Loan Index’s 10-year correlation of 0.65 to equities reflects the credit risk and economic sensitivity of loan issuers. The loan index’s standard deviation of returns (a measure of volatility) is still only one third that of equities, but it’s also higher than the other bond categories. What’s interesting is the loan index’s low correlation to core bonds. “By design, bank loan coupons rise when interest rates go up and, hence, when Treasuries tend to sell off,” write Alec Lucas and Maciej Kowara of Morningstar Manager Research. For this reason, their analysis concludes that bank loans can contribute significantly to the risk/reward profile of a diversified fixed-income portfolio.

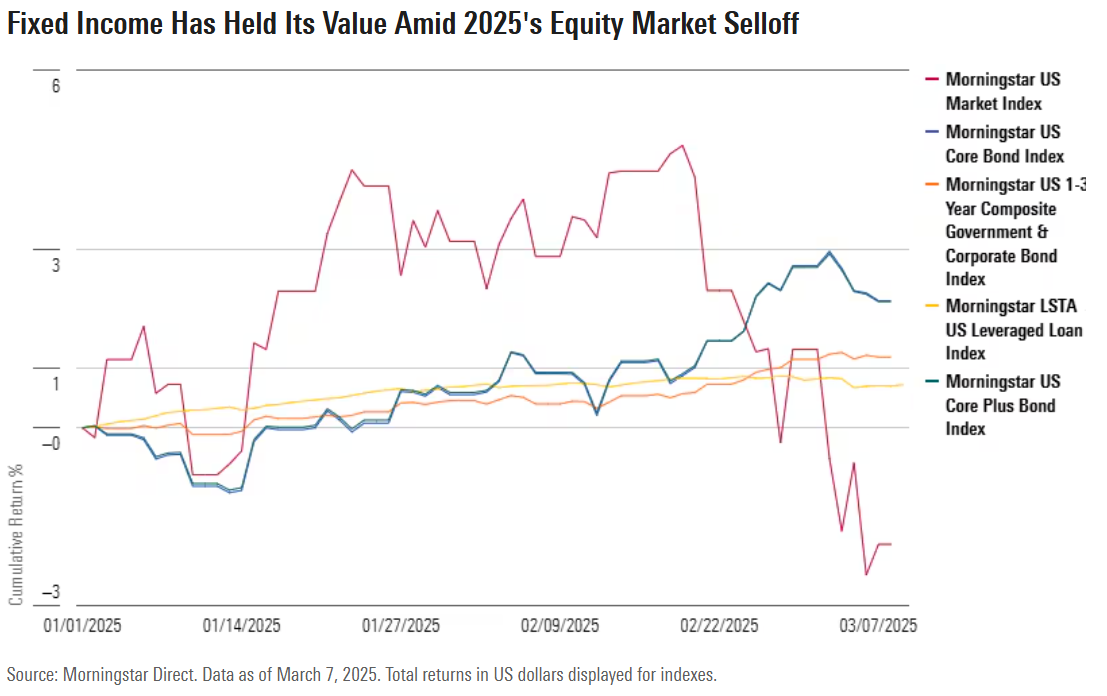

What can recent months tell us about the diversification benefits of fixed income? Policy uncertainty and inflation fears have roiled both stock and bond markets, though, as of this writing, bonds were ahead of stocks in 2025. As displayed below, Morningstar fixed-income indexes were all in positive territory year to date as of March 7, while stocks were down.

Returns will continue to bounce around, and correlations are dynamic. What won’t change is the trade-offs inherent to fixed-income investing. The good news is that, at the current income levels, the outlook for bonds is bright. Noting the uncertainty of equity market forecasting, my colleague Christine Benz writes: “Fixed-income return assumptions are more straightforward given the tight historical correlation between starting yields and returns over the next decade.”

©2025 Morningstar. All Rights Reserved. The information, data, analyses and opinions contained herein (1) include the proprietary information of Morningstar, (2) may not be copied or redistributed, (3) do not constitute investment advice offered by Morningstar, (4) are provided solely for informational purposes and therefore are not an offer to buy or sell a security, and (5) are not warranted to be correct, complete or accurate. Morningstar has not given its consent to be deemed an "expert" under the federal Securities Act of 1933. Except as otherwise required by law, Morningstar is not responsible for any trading decisions, damages or other losses resulting from, or related to, this information, data, analyses or opinions or their use. References to specific securities or other investment options should not be considered an offer (as defined by the Securities and Exchange Act) to purchase or sell that specific investment. Past performance does not guarantee future results. Before making any investment decision, consider if the investment is suitable for you by referencing your own financial position, investment objectives, and risk profile. Always consult with your financial advisor before investing.

Indexes are unmanaged and not available for direct investment.

Morningstar indexes are created and maintained by Morningstar, Inc. Morningstar® is a registered trademark of Morningstar, Inc.